Insurance business planning sits at the intersection of underwriting strategy, capital management and regulatory reporting — yet for most carriers, the tools used to do it have not kept pace with the complexity of modern portfolios. Kompreno is a purpose-built business planning platform designed and built by Describe Data for multi-line insurers and Lloyd’s managing agencies.

Kompreno delivers a fully operational planning environment capable of running 10,000 Monte Carlo simulations in seconds, modelling reinsurance structures, capturing inter-line correlation through copulas, and producing credible aggregate loss estimates at multiple return periods — all through a browser-based interface accessible to underwriters, actuaries and executive stakeholders alike.

Accurate business planning is hard for insurers. Current approaches are either too simple — producing results that lack credibility at board and regulatory level — or too complex, meaning the right questions never get answered quickly enough to inform decisions.

In practice, planning cycles for most Lloyd’s syndicates and managing agencies are still driven by a combination of Excel workbooks and legacy internal tools. Four specific problems are almost universal:

Spreadsheet fragility. Planning models grow organically over years, with assumptions embedded across dozens of sheets and no automated testing. Small changes require careful manual propagation, and errors surface late — sometimes after board sign-off.

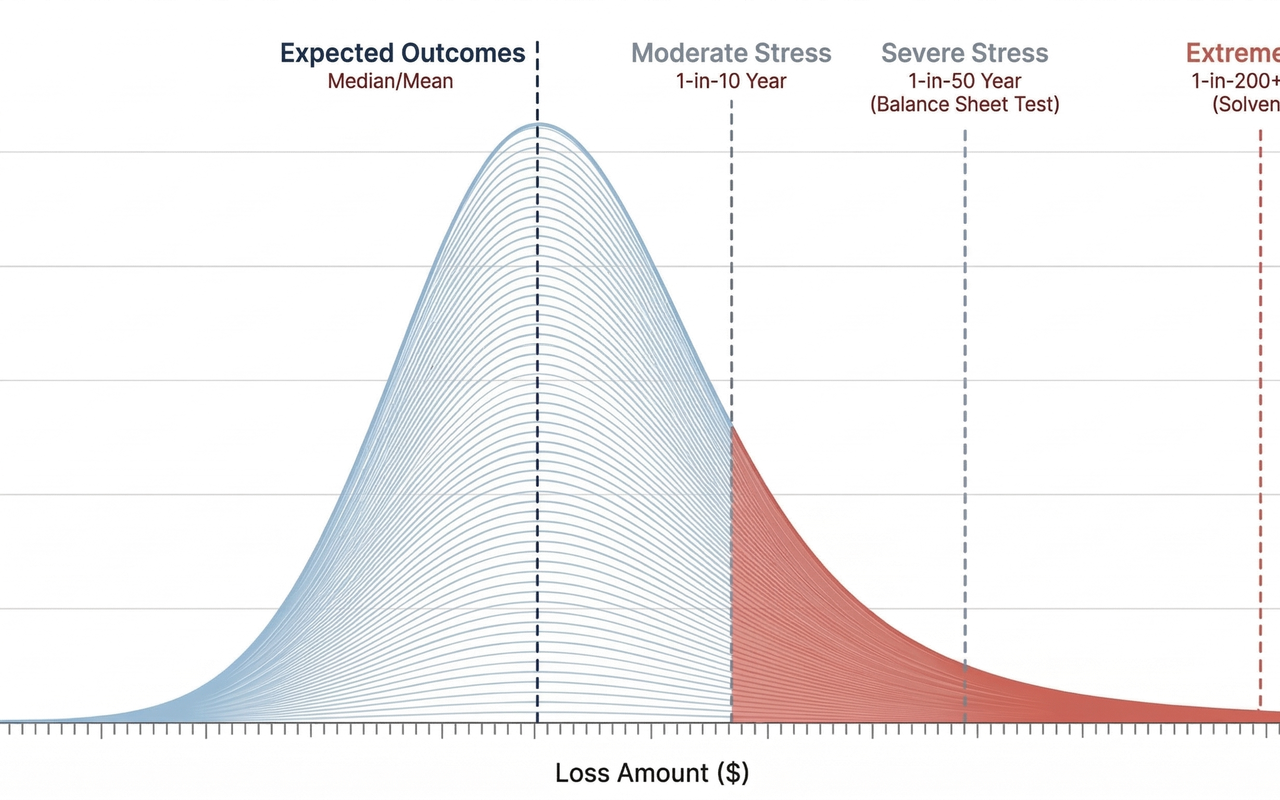

No treatment of correlation. Most models combine line-level loss estimates by simple addition, with a manual correlation adjustment applied as a single scalar at the aggregate level. This approach systematically underestimates tail exposure: it ignores the non-linear dependence between lines that only becomes visible at the extremes — precisely when it matters most for capital adequacy.

Slow cycle times. Running a single scenario to completion takes hours. Testing a range of reinsurance structures, or stress-testing the plan against a hardening or softening market, is impractical within a normal planning window. As a result, the range of scenarios actually examined stays narrow.

Limited accessibility. The model is effectively a single-user system. Underwriting heads who want to understand the capital implications of a change to their book must route requests through the actuarial team, introducing lag and reducing the quality of strategic conversation at the senior level.

Kompreno is a cloud-hosted platform that addresses each of these constraints directly.

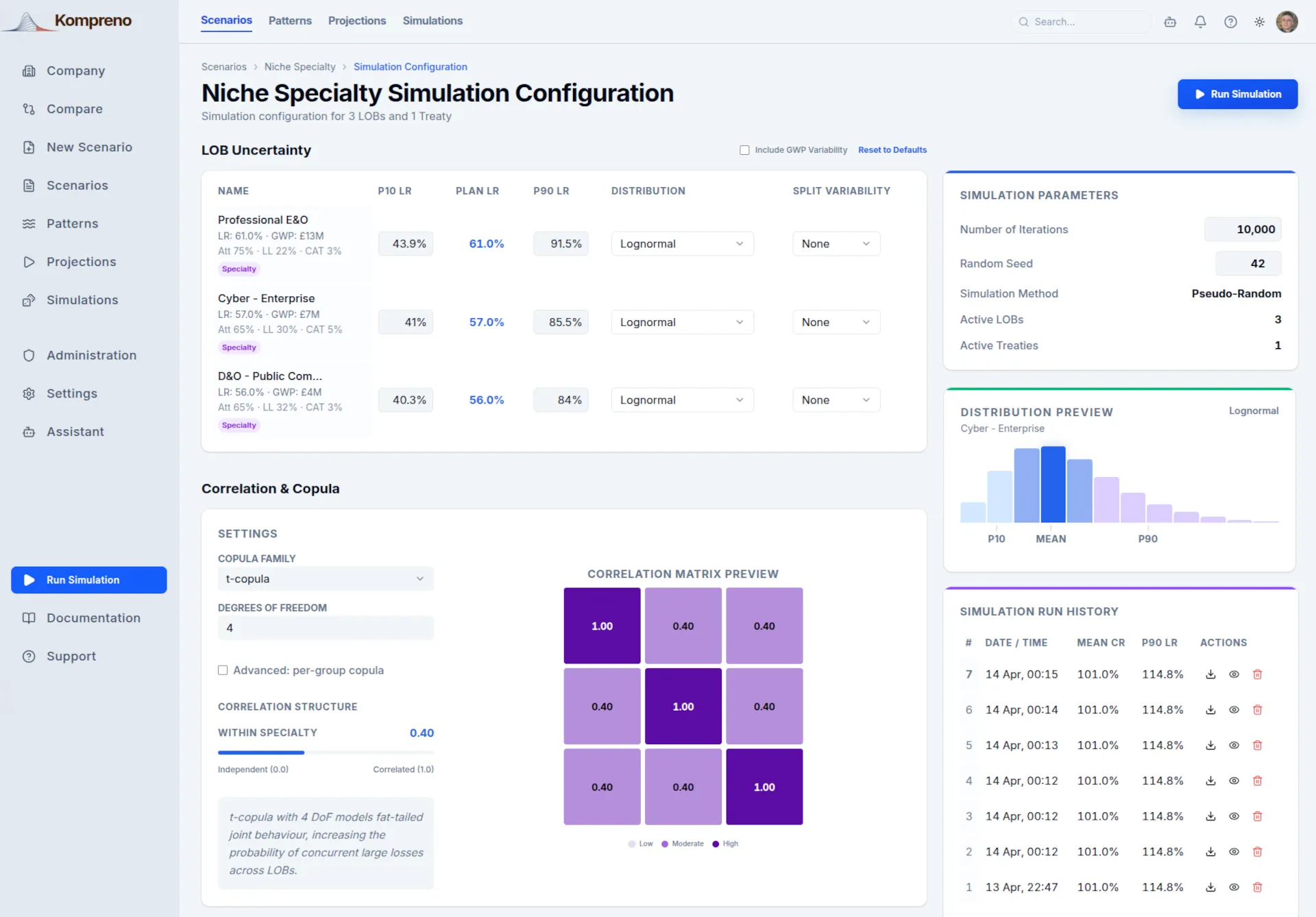

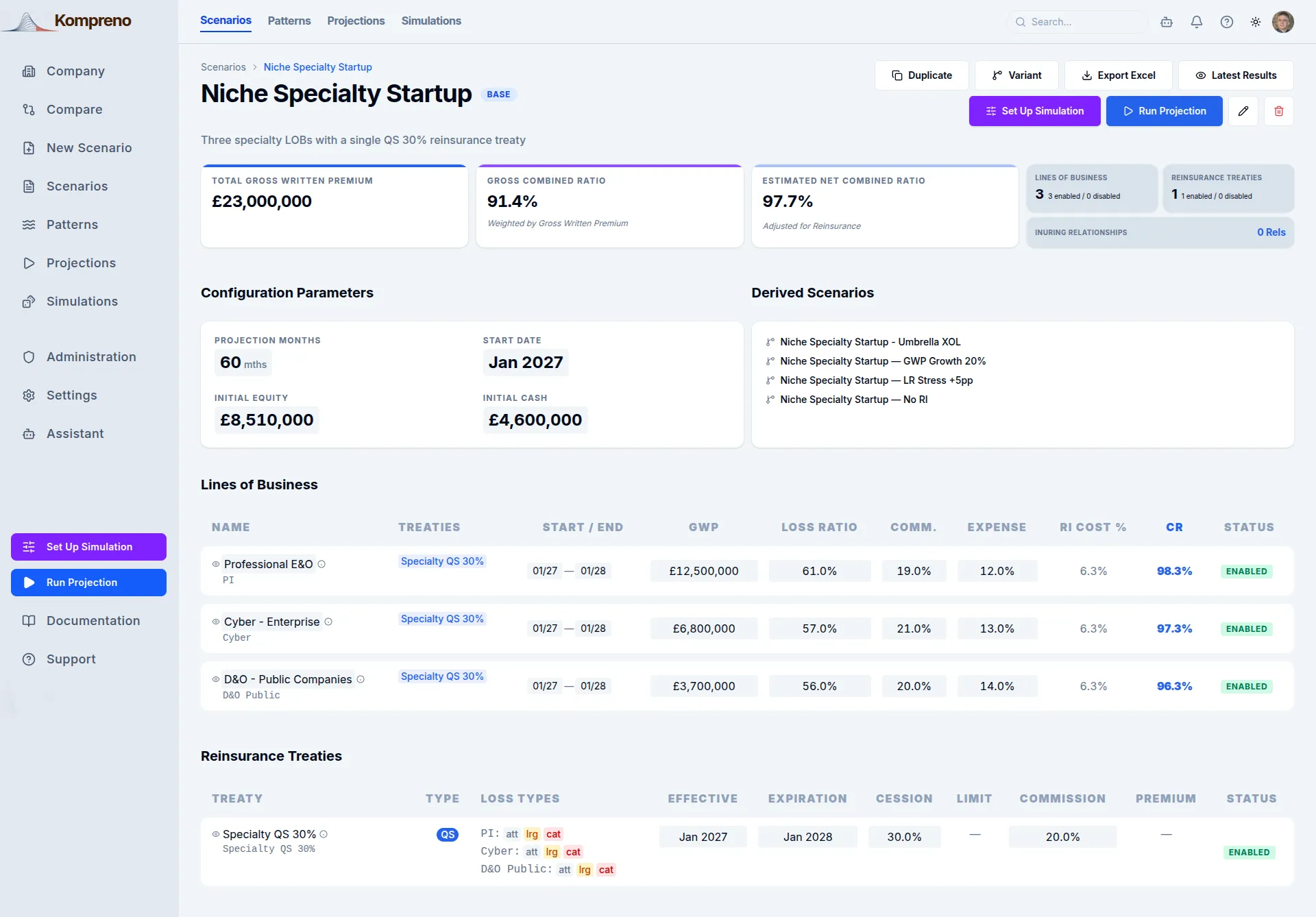

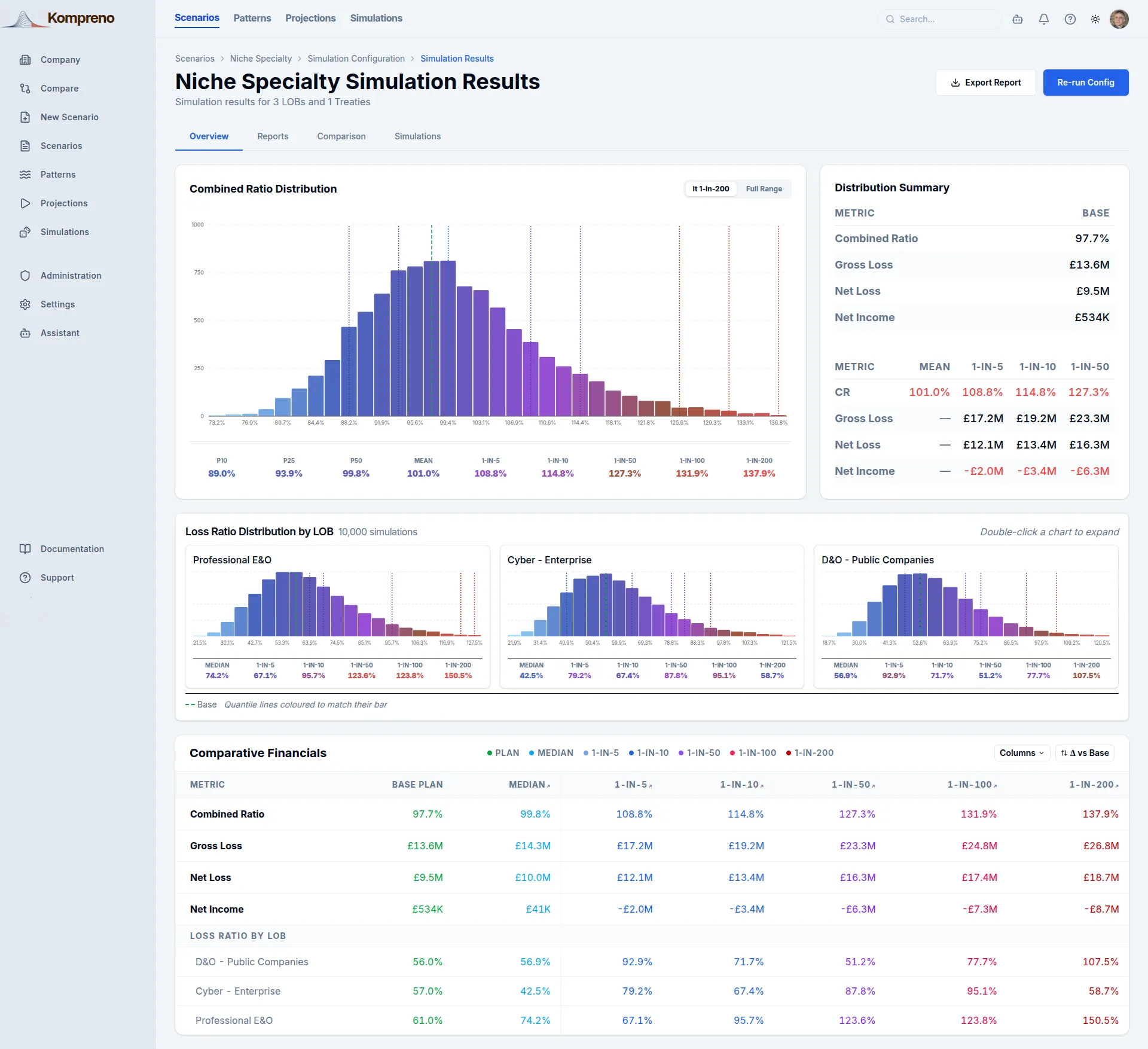

Simulation Engine. The foundation of Kompreno is a stochastic simulation engine that generates 10,000 full-year scenarios per run, each producing a complete set of monthly financial statements — gross written premium, net earned premium, attritional and large loss components, reinsurance recoveries, expenses, and balance sheet movements. Each simulation is self-consistent: cash flows balance, reinsurance recoveries are applied correctly at the right trigger points, and outputs are auditable at the individual scenario level.

Copula-Based Correlation Modelling. The treatment of inter-line correlation is the most technically significant component of the platform. Kompreno models the joint loss distribution across lines of business using copulas, which capture dependence structures that linear correlation coefficients miss entirely. A Gaussian copula captures average co-movement; a Student-t or Clayton copula captures tail dependence — the tendency for multiple lines to deteriorate simultaneously in stress scenarios. The result is that 1-in-100 and 1-in-200 aggregate estimates reflect genuine tail dependence, not a scaled-up average — a material difference for portfolios where a major property catastrophe also drives liability and marine losses through supply chain and business interruption effects.

Scenario and Reinsurance Configuration.

Underwriters and actuaries can configure scenarios interactively — adjusting line-level premium budgets, loss ratio assumptions, rate change expectations and reinsurance programme structures — and run comparisons side by side. Reinsurance structures supported include excess-of-loss treaties (per-risk and per-occurrence), quota share arrangements and aggregate covers, with reinstatement premiums, co-insurance and sliding scale commissions all handled correctly within the simulation.

Scenario Detail and Drill-Down.

Every aggregate output is traceable back to the individual simulation that produced it. When the platform reports that the 1-in-10 aggregate loss is £4.2m, an underwriter can drill into exactly which scenarios constitute that percentile, examine the line-level contributions, and understand which combination of attritional frequency, large loss severity and inter-line correlation drove the outcome — essential for Lloyd’s reporting and for building confidence in model outputs at board level.

Simulation Results and Return Period Analysis.

The results interface presents loss distributions, return period exceedance curves and financial performance metrics — combined ratio, ROE, solvency coverage — at multiple percentiles. Reinsurance structures can be compared head-to-head on risk-adjusted return: the platform can answer a question like “does a 60% quota share on Casualty outperform the XOL alternative on ROE at the 75th percentile, accounting for tail volatility?” in seconds, rather than days.

Kompreno reflects a broader principle in insurance technology: the limiting factor on the quality of strategic decision-making is often not the availability of analytical talent, but the cost and latency of accessing analytical outputs. When the infrastructure makes it cheap to ask questions, the questions asked are better ones.

Proper tail modelling matters. For multi-line portfolios, the difference between a linear correlation assumption and a properly calibrated copula is not a theoretical nicety — it is a material difference in the estimated probability of capital-threatening events. Getting this right requires both statistical methodology and deep familiarity with the specific correlation drivers in insurance: catastrophe overlap, macro-economic stress, litigation cycle co-movement. Kompreno embeds that expertise directly into the platform.